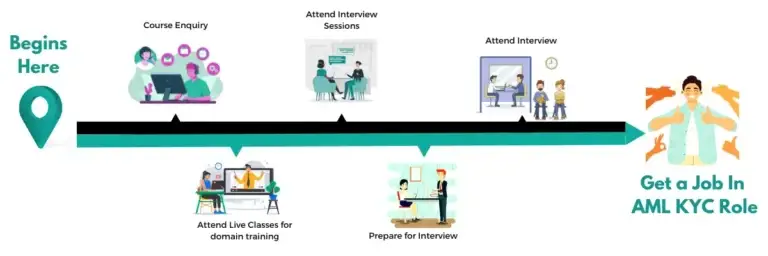

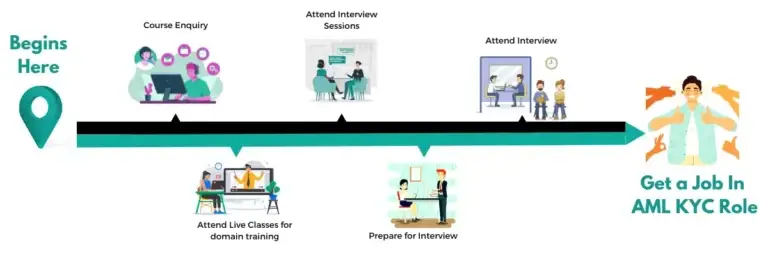

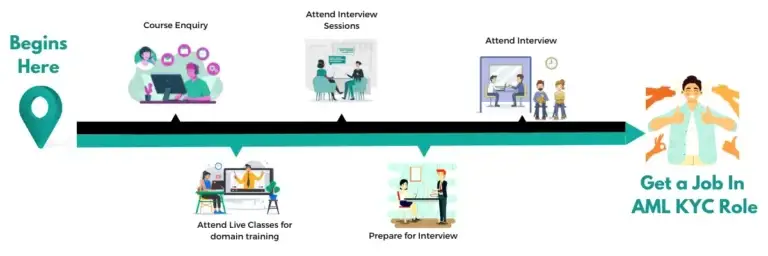

Corporate AML KYC Interview Question and Answers

Last Updated on Aug 28, 2025, 2k Views

Corporate Aml kyc interview question and answers

1. What is the purpose of KYC and AML regulations?

Sample Answer:

KYC and AML regulations are designed to prevent financial institutions from being used for money laundering, terrorist financing, and other illegal activities. KYC ensures that institutions verify and understand the identity of their clients, while AML involves ongoing monitoring and reporting of suspicious activities. Together, they help maintain the integrity of the financial system.

2. What documents are typically required for KYC compliance for a corporate client?

Sample Answer:

For a corporate entity, KYC documentation usually includes:

Certificate of incorporation

Memorandum and Articles of Association

List of directors

Shareholder register and ownership structure

Proof of address of the business

IDs and proof of address for UBOs (Ultimate Beneficial Owners)

Board resolution authorizing the signatories

The exact requirements may vary depending on the jurisdiction and the bank’s internal policies.

3. How do you identify and verify Ultimate Beneficial Owners (UBOs)?

Sample Answer:

UBOs are individuals who ultimately own or control more than a certain percentage (often 25%) of a company. To identify UBOs, we review the shareholding structure and request supporting documents like shareholder registers or organizational charts. Verification involves obtaining and validating identity documents and conducting screening for PEP status or negative media.

4. What is Enhanced Due Diligence (EDD) and when is it required?

Sample Answer:

Enhanced Due Diligence is a more detailed review process used when a client poses a higher risk, such as a politically exposed person (PEP), a client from a high-risk jurisdiction, or those with complex structures. EDD involves additional steps like deeper background checks, more frequent reviews, and possibly senior management approval.

5. How do you perform a risk assessment of a client?

Sample Answer:

A client risk assessment considers factors such as the type of client (individual, corporate, trust), geographical risk, industry/sector risk, product/service usage, transaction patterns, and the client’s ownership structure. These are evaluated using a risk rating tool or framework to classify the client as low, medium, or high risk.

6. What is a PEP and how do you handle PEP clients?

Sample Answer:

A PEP, or Politically Exposed Person, is someone who holds or has held a prominent public position (e.g., government official, judge, military officer). Due to their position, they may pose a higher risk of corruption. When dealing with PEPs, EDD is mandatory, including senior management approval and more frequent monitoring.

7. What steps do you take when identifying suspicious transactions?

I look for red flags such as large cash deposits, rapid movement of funds without a clear purpose, transactions inconsistent with the client’s profile, or activity involving high-risk jurisdictions. When suspicious activity is identified, it is documented and escalated to the compliance team for further investigation, and possibly a SAR (Suspicious Activity Report) is filed.

8. What tools or systems have you used for screening or KYC checks?

Sample Answer:

I’ve worked with screening and onboarding tools like World-Check, Dow Jones Risk & Compliance, LexisNexis, and internal KYC platforms. These tools help with sanctions, PEP, and adverse media screening. For document verification and workflow tracking, I’ve also used systems like Salesforce, Actimize, or Fenergo, depending on the organization.

9. How do you stay updated on AML and KYC regulations?

I regularly follow regulatory updates from FATF, FinCEN, OFAC, and local financial regulators. I also subscribe to compliance newsletters, attend webinars, and participate in training provided by ACAMS or internal compliance teams to stay current with global and regional changes.

10. Describe a challenging KYC case you handled and how you resolved it.

Once, we had a corporate client with a multi-tiered ownership structure involving multiple jurisdictions, including offshore entities. It was challenging to trace the UBOs due to lack of transparency in some jurisdictions. I collaborated with our legal team, used registry searches, and engaged external data providers to trace ownership. We finally identified two UBOs and completed EDD. This case underscored the importance of persistence and cross-functional teamwork.

11. How do you handle conflicting deadlines between onboarding multiple high-risk clients?

I prioritize based on risk level and business impact. High-risk clients may require more time for EDD, so I initiate that process early while continuing with standard KYC reviews for lower-risk clients. I also communicate timelines clearly with internal stakeholders and request additional support if needed.

12. What would you do if a client refuses to provide required KYC documents?

I would explain the regulatory necessity of the documents and offer support in understanding or gathering them. If they still refuse, I escalate the case to compliance and halt onboarding or continue the exit process if they’re an existing client, as per policy.

Career Advice!

Feel Free to Contact Us or WhatsApp Us for Career Counseling!

- +91 9066508122

Learning Journey

Data Science Interview Questions

Data Science Interview Questions Data Science Interview Questions 1. What...

Read More

Top 30 DevOps Interview Questions & Answers (2022 Update)

Top 30 DevOps Interview Questions & Answers (2022 Update) Top...

Read More

Anti Money Laundering Interview Questions

Anti Money Laundering Interview Questions Anti Money Laundering Interview Questions...

Read More