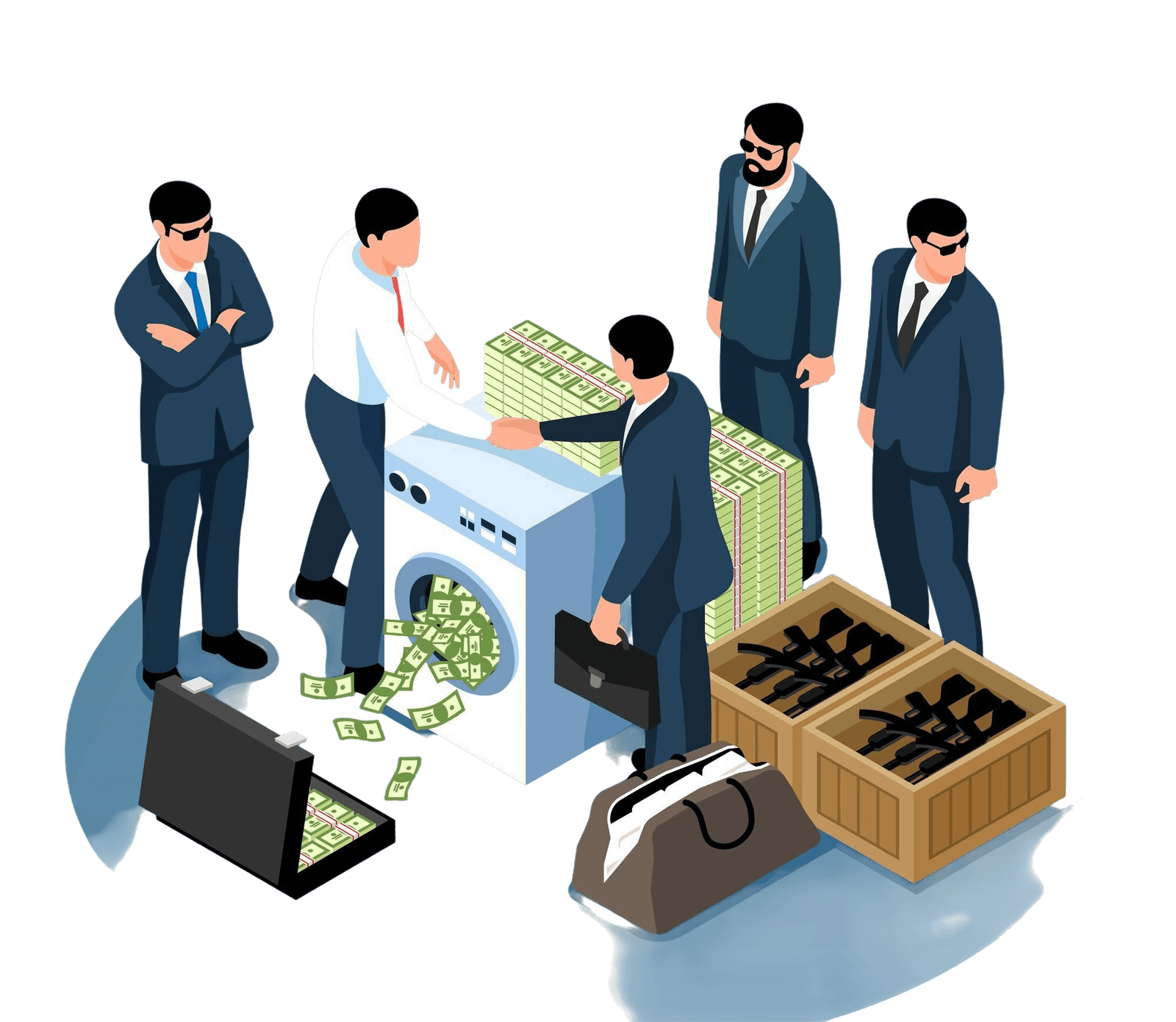

1️⃣ What is Money Laundering?

Money laundering is the process of making illegally obtained money appear legitimate. It usually happens in three stages:

Placement – Introducing illegal money into the system

Layering – Moving money through multiple transactions to hide its origin

Integration – Reintroducing the money as “clean” funds

Non-financial businesses are often used in the placement and integration stages.

2️⃣ Which Non-Financial Businesses Are Covered Under AML?

These are often called DNFBPs (Designated Non-Financial Businesses and Professions):

✔ Real Estate Agents

Property purchases are commonly used to launder large amounts of money.

✔ Lawyers & Notaries

Especially when handling:

Client funds

Company formation

Property transactions

✔ Accountants

Can unknowingly help structure transactions to hide funds.

✔ Company Formation Agents

Used to create shell companies.

✔ Casinos & Gaming Businesses

Cash-heavy operations are high risk.

✔ Dealers in High-Value Goods

Luxury cars

Jewelry

Art

Precious metals

High-end electronics

✔ Trust & Company Service Providers

3️⃣ AML Obligations for Non-Financial Businesses

Even if not a bank, businesses may be required to implement:

🔎 1. Customer Due Diligence (CDD)

- Verify identity (KYC – Know Your Customer)

- Understand nature of business relationship

- Identify beneficial owners

📄 2. Record Keeping

- Maintain customer records

- Keep transaction documentation (usually 5–10 years)

🚨 3. Suspicious Transaction Reporting (STR)

- Report suspicious activities to authorities (FIU – Financial Intelligence Unit)

⚖ 4. Risk-Based Approach

- Conduct AML risk assessment

- Apply enhanced due diligence for high-risk customers

📚 5. Internal Controls

- Appoint AML compliance officer

- Staff training

- Written AML policies & procedures

4️⃣ Why AML Matters for Non-Financial Businesses

Failure to comply can result in:

Regulators globally (FATF guidelines) require countries to monitor non-financial sectors due to increasing misuse.www