Data Science Interview Questions Data Science Interview Questions 1. What...

Read More

AML (Anti-Money Laundering) refers to laws, regulations, and procedures designed to prevent criminals from disguising illegally obtained funds as legitimate income.

Banks and financial institutions are the primary gatekeepers of the financial system, making AML compliance a critical function.

Banks are vulnerable because they:

Handle large volumes of transactions

Offer cross-border transfers

Provide accounts, loans, investments, and trade finance

Enable digital and online payments

Without AML controls, banks can be used for:

Money laundering

Terrorist financing

Fraud and corruption

Tax evasion

Sanctions evasion

Regulatory penalties for non-compliance can include:

Heavy monetary fines

License cancellation

Criminal liability

Severe reputational damage

🇮🇳 India

Prevention of Money Laundering Act (PMLA), 2002

RBI AML/KYC Master Directions

Financial Intelligence Unit – India (FIU-IND)

🌍 Global

FATF (Financial Action Task Force) Recommendations

USA PATRIOT Act (U.S.)

EU AML Directives

Basel Committee Guidelines

1. Customer Due Diligence (CDD)

Also called KYC (Know Your Customer).

Includes:

Customer identification & verification

Address proof & identity proof

Beneficial ownership identification

Risk categorization (Low/Medium/High risk)

Enhanced Due Diligence (EDD) for:

Politically Exposed Persons (PEPs)

High-risk countries

High-value clients

2. Transaction Monitoring

Banks use automated systems to detect suspicious patterns like:

Large cash deposits

Structuring (smurfing)

Rapid movement of funds

Unusual international transfers

Transactions inconsistent with customer profile

3. Suspicious Transaction Reporting (STR)

If suspicious activity is detected:

Bank files STR with FIU-IND (in India)

Confidential process (customer not informed)

Mandatory reporting timelines

4. Sanctions Screening

Screening against:

UN sanctions lists

OFAC lists

Domestic watchlists

Terrorist databases

5. Record Keeping

Maintain customer records for 5–10 years

Maintain transaction history

Ensure audit trails

6. Ongoing Monitoring

AML is not a one-time process.

Banks must:

Periodically update KYC

Reassess risk

Monitor unusual behavior continuously

Retail Banking

Corporate Banking

Correspondent Banking

Trade Finance

Private Banking

Digital/Neo Banks

Cryptocurrency exposure

Roles :

Board of Directors

Board of Directors

AML Analysts

Relationship Managers

Relationship Managers

Responsibilities:

Approve AML policy

Oversee AML program

Investigate alerts

Perform CDD

Test AML controls

Modern banks use:

AI & Machine Learning

Behavioral analytics

Name screening tools

Transaction monitoring systems

Case management systems

False positives in monitoring

Cross-border regulatory differences

Increasing digital fraud

Shell companies & layered transactions

Cryptocurrency risks

Major global banks have paid billions in fines for:

Weak monitoring systems

Failure to report suspicious activity

AML in banking ensures:

✔ Financial system integrity

✔ Prevention of crime & terrorism

✔ Regulatory compliance

✔ Institutional reputation protection

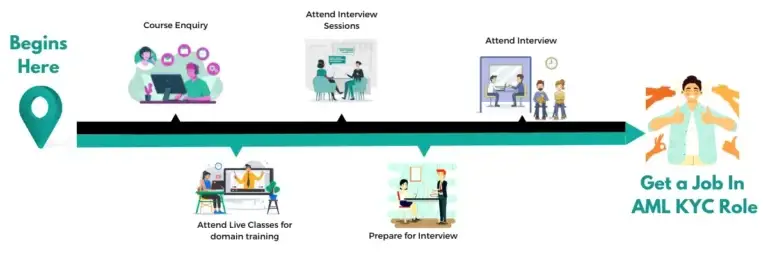

Feel Free to Contact Us or WhatsApp Us for Career Counseling!

Data Science Interview Questions Data Science Interview Questions 1. What...

Read MoreTop 30 DevOps Interview Questions & Answers (2022 Update) Top...

Read MoreAnti Money Laundering Interview Questions Anti Money Laundering Interview Questions...

Read More

“Education is the most Powerful Weapon for Future”

Job Guarantee Courses:

Anti Money Laundering | Digital Marketing | RPA UiPath | IoT | Automation Testing Course Using Python or Java | PCB Design | Embedded System | Data Science | AWS Cloud Computing |

Trending Certification IT Courses:

Anti-Money Laundering Certification Course | Digital Marketing Certification Course | RPA UiPath Certification Course | Python Certification Course | IoT Certification Course |IoT Certification Course | Automation Testing Course Using Python or Java | PCB Design Course Certification | Embedded System Certification Course | Data Science Certification Course | AEM Certification Course | AWS Cloud Computing Certification Course |

©2026-27 dridhOn Services & Solutions. All Rights Reserved.

DISCLAIMER: THE NAMES OF THE CERTIFICATIONS ARE THE TRADEMARKS OF THEIR OWNERS.